This Doomsday Law Could Stop Trains Across America In A Matter of Weeks

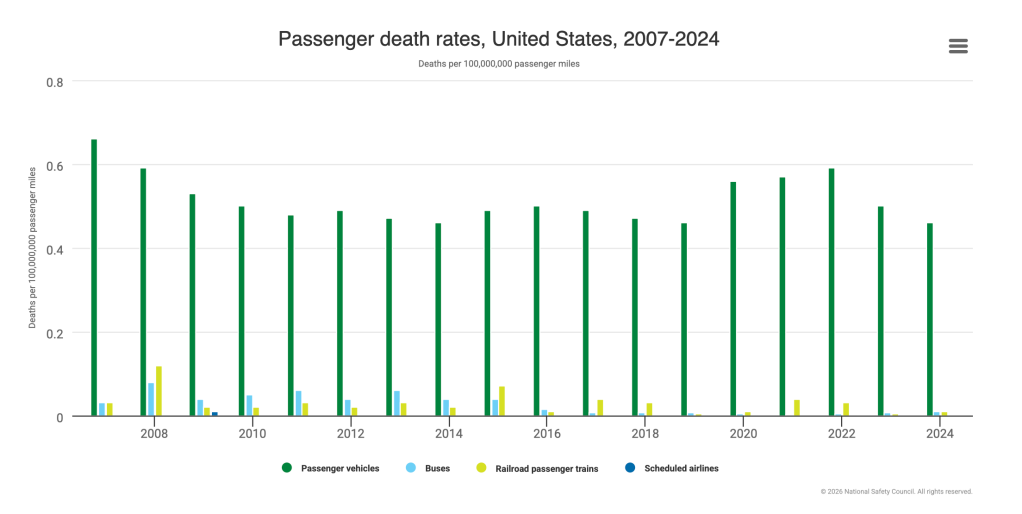

A little-known federal insurance requirement could soon bring American trains to a halt — even though commuter rail is far safer than other modes of travel.

The commuter railroad industry is bracing for the impending publication of a new federal “passenger rail liability cap,” which will start a 30-day doomsday clock for every rail operator in America to either secure millions of dollars in additional insurance, or immediately cease operations.

Even more troubling: It’s unclear whether the insurance industry will be able to issue the requisite policies. Experts said it almost certainly won’t.

Rail advocates have repeatedly warned that global insurance companies have struggled for years to write policies for railroads, thanks to a rise in climate change-related claims straining the insurance market as a whole and the sheer scale of the liability coverage that Congress forces railroads to secure.

Worse, the level of those liability caps has little to do with the actual probability of insurable incidents, which is significantly lower than cars. And because many rail fans are unfamiliar with the wonky world of underwriting, few have spoken up about a potentially existential threat to their favorite mode of getting around.

“What we really need is a public groundswell,” said Jim Mathews, President and CEO of the National Rail Passengers Association. “You need the public to comment in the docket and send letters to their members of Congress … Regular people [need to know that] train services are potentially threatened because very safe train operators, who have never had a wreck, are facing the reality that their insurance is going to go up — just because the law says it has to. And the insurance market doesn’t want to do it.”

How we got here

The rail industry’s looming insurance crisis traces back to 1997, when the Amtrak Reform and Accountability Act first mandated that railroads secure $200 million in excess liability insurance to cover the maximum allowable settlement that all passengers can secure from a single incident. (That requirement also functioned as the minimum allowable liability insurance policy railroads can hold and still run trains, making the “cap” both a ceiling and a floor.)

At the time, the number seemed fair to many rail advocates, who recognized that serious train crashes are rare compared to serious car crashes, but can be devastating and costly for surrounding communities. What wasn’t fair, though, was how the cap continued to increase — even if the number of train crashes held steady.

Under the FAST Act of 2015, the liability cap ballooned to $294 million — a development some advocates attributed to the influence of trial lawyers chasing bigger settlements rather than any meaningful analysis of the current costs of railway disasters.

“[It’s] a little self serving, if I will say,” said KellyAnne Gallagher, CEO of the Commuter Railway Coalition. “The more that railroads have to carry, the higher a trial lawyer can push for a jury verdict.”

Worse, federal law requires Congress to adjust the cap every five years; in 2021, the legislative body raised it to $323 million. The next adjustment is due any day now, and advocates believe the cap will rise to around $400 million — an increase of nearly 24 percent.

Some larger carriers will be able to adjust their budgets to cover the gap; smaller carriers, who are already paying a tenth or more of their budget on insurance, may not be so lucky.

Other modes of travel, meanwhile, have it far easier. The liability cap for freight truck companies, for instance, hasn’t budged since Congress set it at just $750,000 in 1980 — a staggering 46 years ago. This is particularly notable given the surging number and associated costs of truck crashes, which often leave victims and survivors destitute, especially when a big rig causes a grisly, multi-car pile-up with damages comparable to train crashes.

Furthermore, the federal government imposes zero liability minimums on the individual drivers of passenger cars, who cause the vast majority of transportation tragedies in America, and largely leaves insurance matters up to the states. Legislators in New York are actually working to reduce motorists’ insurance costs, even as advocates warn that crash victims will pay the price.

How a broken insurance market is getting worse

Even if the pending liability cap increase is arbitrary, both Mathews and Gallagher said that railroads have tried to prepare to pay it. If the insurance market isn’t ready to provide the necessary policies, however, rail operators may not be able to secure new policies anyway, which could take the trains entirely offline.

Mathews explained that, due to the sheer size of the liability coverage that railroads are obligated to secure, no single insurance company can afford to offer them a single, comprehensive policy. That forces operators to cobble together insurance “towers” of more than a dozen different policies that collectively reach the federal cap.

Because there are simply not enough American insurers to fully assemble these teetering “towers,” railroads are forced to rely on foreign insurance markets in places like Bermuda and London to cover the gap. That means a significant portion of railroad budgets, most of which heavily rely on local tax receipts, flow directly to overseas entities — all because Congress dictated an arbitrarily high liability cap.

“Even when we’ve gone on the Hill and pointed out how much has to be spent overseas to acquire this insurance, it doesn’t seem to resonate that tax dollars are being sent abroad,” Gallagher added. “We would have thought that that would be a trigger, and it hasn’t really triggered anyone.”

With the insurance market across all sectors buckling under the weight of climate disasters, Mathews fears the Londons and Bermudas of the world will think twice before insuring a U.S. railroad. If that happens, and Congress doesn’t relax its unrealistic standard, American trains could stop rolling.

“Wildfires in Madagascar will affect the rate that you as a commuter operator in San Diego are paying for insurance,” he told Streetsblog. “We’re reaching a point where the insurance market just does not want to sell policies to these railroads anymore. And as the cap gets higher, the insurance just becomes out of reach.”

What to do — and why to do it now

An industry-wide insurance crisis would be a disaster for commuter rail passengers. But Gallagher said it would be a particular tragedy given the mode’s recent gains in service and ridership.

Commuter rail largely recovered its pre-pandemic ridership by 2024, and some systems, like Caltrain, even doubled weekend passenger counts. Railroads have made massive investments in safety since the cap was last raised, too, and they’re just starting to record the long-term benefits of innovations like “positive train control” systems, which advocates said make trains safer every year they operate.

Rail advocates hoped that this summer’s World Cup games would be an opportunity to show the world how far we’ve come on the rails. They now wonder if trains will run at all.

“We would have hoped that market forces would have had a positive impact on the premiums we pay for this insurance,” added Gallagher. “We would have hoped that a drop in ridership during COVID would have had a positive impact on the premiums. It is not so … Our safety record and our safety investments have no bearing [on what we pay].”

As Congress drafts the next major federal transportation bill, Gallagher is lobbying legislators to defer the recalculation of the liability cap by four years, and to provide railroads (and the overwhelmed insurance market) year to comply with it.

Mathews said Congress could explore more radical solutions, too, such as requiring the Federal Railroad Administration to use actuarial science when estimating the costs of rail disasters, and creating tiered minimums to accommodate a diverse range of operators. Authorizing state-level transportation departments and commuter rail agencies to create their own insurers to pool risks regionally is another idea he supports; so is the creation of a “risk-sharing backstop” at the federal level, and giving the Surface Transportation Board more power to help set fair requirements rather than forcing Congress into the weeds on such a complex issue.

As wonky as all that might sound, though, Mathews said the stakes of this conversation couldn’t be higher — and the time to call your Congressional representative is now.

“It’s very esoteric and nerdy, and people don’t really want to talk about insurance because it seems bizarre,” he added. “But at the same time, you’re going to care if your commuter operator has to suspend service because they can’t get insured.”

Read More:

Streetsblog has migrated to a new comment system. New commenters can register directly in the comments section of any article. Returning commenters: your previous comments and display name have been preserved, but you'll need to reclaim your account by clicking "Forgot your password?" on the sign-in form, entering your email, and following the verification link to set a new password — this is required because passwords could not be carried over during the migration. For questions, contact tips@streetsblog.org.